Commerzbank increases net profit for 2023 to €2.2 billion

Strategy is delivering

02/15/2024

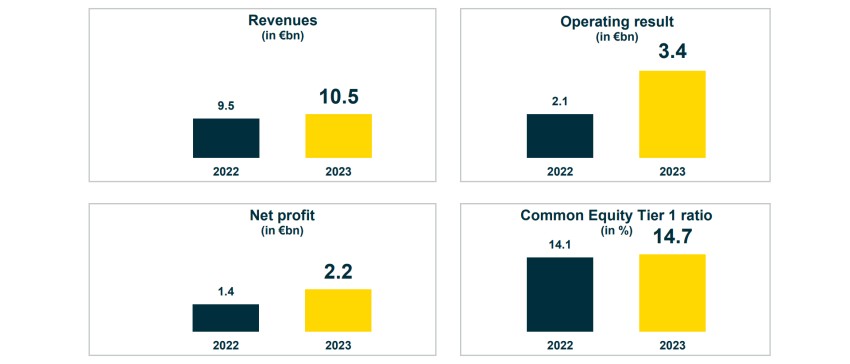

- Operating result increased by more than 60% to €3.4 billion in 2023 (2022: €2.1 billion) – net profit increased by 55% to €2.2 billion

- Strong customer business and interest rate development lead to very strong net interest income and revenues increased to €10.5 billion (2022: €9.5 billion)

- Costs reduced to €6.4 billion (2022: €6.5 billion) – cost-income ratio significantly improved to 61% (2022: 69%)

- Decreased risk result of minus €618 million despite economic slowdown (2022: minus €876 million) – low non-performing loan ratio of 0.8%

- Capital distribution of €1 billion for 2023 financial year planned – targeted dividend of around 35 cents per share complements ongoing share buy-back programme

- Outlook 2024: net profit above 2023 levels and pay-out ratio of at least 70% targeted, but not more than net profit

Commerzbank increased its net profit by more than 50% to €2.2 billion in the 2023 financial year. As a result, the Bank not only achieved a net profit well above that of the previous year but also generated its best result in 15 years. Despite high special burdens in Poland of around €1.1 billion, the operating result rose by more than 60% to €3.4 billion. The Bank benefited from strong customer business and persistently high interest rates. Net interest income climbed to €8.4 billion. Net commission income contributed around €3.4 billion to the Bank’s revenues. The loan portfolio proved to be very robust, despite the continuing difficult economic environment. The risk result fell by around 30%, and the non-performing loan ratio was only 0.8%. The CET 1 ratio improved over the course of the year to 14.7%, which puts the Bank comfortably above of the regulatory minimum requirement.

The excellent overall annual result enables the Bank to return capital to its shareholders. Overall, the Bank is planning a pay-out ratio of 50% of net profit after deduction of AT1 coupon payments. Currently, a share buy-back programme with a volume of up to €600 million is under way. In addition, the Bank intends to distribute a dividend of around 35 cents per share, subject to the approval of the Annual General Meeting.

“Commerzbank had an excellent financial year 2023. We delivered on the key objectives of our ‘Strategy 2024’ ahead of schedule and in some areas we even exceeded them. On this basis, we will achieve a further increase in net profit for the current year”, said CEO Manfred Knof. “The goals we have set ourselves with our strategy 2027 are ambitious, but achievable. That’s why we’re now moving full steam ahead with the implementation. We want to broaden our revenue base and thus become less dependent on net interest income. In sales, we have made a very strong start to the new year in both customer segments. This confirms our strategy and gives us additional tailwind.”

The implementation of Commerzbank’s strategic plan until 2027 is already showing initial signs of success. In line with the strategic pillars of growth, excellence, and responsibility, the Bank has set itself the goal of providing each customer with a tailor-made offering that meets their individual needs. This includes further developing its payment transaction solutions and launching a joint venture, Commerz Globalpay GmbH, to offer digital payment products to business customers in Germany. The product offering will include, for example, a smartphone-based payment application that enables retailers to accept mobile payments without a separate card reader.

The Bank is also stepping up its growth in the field of sustainability. With the agreed majority stake in Aquila Capital Investmentgesellschaft based in Hamburg, Commerzbank is significantly expanding its sustainable asset management offerings. The investment company specialises in real asset-based investments, such as renewable energy and sustainable infrastructure projects. This investment opens up growth opportunities for the Bank and will have a positive impact on its commission income. The transaction is subject to the approval of the regulatory authorities.

In the Corporate Clients segment, Commerzbank has expanded its successful collaboration with ODDO BHF as an exclusive partnership in the field of Equity Capital Markets (ECM) for the Swiss market. In Switzerland – a key part of our DACH home market – Commerzbank will now be able to offer equity research for around 50 listed companies and provide its customers with the full ECM product range.

Strong customer business delivers record result in 2023 financial year

Commerzbank increased its revenues in the 2023 financial year by around 11% to €10.461 billion (2022: €9.461 billion), supported by strong customer business and a sustained tailwind from higher interest rates. Once again, this includes high special burdens due to provisions for legal risks from Swiss franc loans at the subsidiary mBank in Poland. In 2023, these totalled €1.094 billion (2022: €650 million). Net interest income rose by a third to €8.368 billion (2022: €6.459 billion), while net commission income was slightly down at €3.386 billion (2022: €3.519 billion).

Commerzbank continued its strict cost discipline in 2023 and reduced its total costs to €6.422 billion (2022: €6.486 billion). High inflationary pressure as well as expenses for inflation compensation payments and higher provisions for variable compensation due to the good result were partially offset by the Bank through active cost management. As a result, operating expenses increased to €6.006 billion (2022: €5.844 billion). In turn, compulsory contributions fell to €415 million (2022: €642 million) due to a lower European bank levy compared to the previous year and lower contributions to the deposit guarantee scheme in Poland. The cost-income ratio continued to improve significantly over the full year to 61% (2022: 69%).

Despite the ongoing effects of the war in Ukraine and the weak economy with rising insolvencies, the risk result in 2023 was significantly lower than in the previous year, at minus €618 million due to releases (2022: minus €876 million). The Bank also continues to maintain an additional general risk provision (Top-Level Adjustment, TLA) of €453 million, which is available for expected secondary effects, such as supply chain disruptions and uncertainties due to inflation, and the effects of the current restrictive monetary policy. The quality of the loan book continues to be very high with a non-performing loan ratio (NPE ratio) of just 0.8% at the end of the year.

Overall, Commerzbank increased its operating result by more than 60% to €3.421 billion in the past financial year (2022: €2.099 billion). Net profit also rose accordingly: compared to the previous year, net profit after taxes and minority interests increased by 55% to €2.224 billion (2022: €1.435 billion).

The Common Equity Tier 1 ratio (CET 1 ratio) once again increased to a very comfortable 14.7% as of 31 December 2023 (December 2022: 14.1%). The accrual for the planned capital return is already reflected in this. The buffer to the regulatory minimum requirement, based on SREP requirements effective from 1 January 2024, of around 10.3% was 435 basis points. Return on equity (RoTE) improved significantly to 7.7% (2022: 4.9%) at the end of the financial year, with the Bank already exceeding the previous target of 7.3% set for 2024.

Due to the strong business result, Commerzbank plans to return a total of around €1 billion of capital to its shareholders. This corresponds to the target set out in the capital return policy of returning 50% of its net profit for 2023 after deduction of the AT1 coupon payments. Part of the capital return is the current share buy-back programme with a volume of up to €600 million. In addition, the Board of Managing Directors is planning a dividend payment of around 35 cents per share, which is subject to approval by the Annual General Meeting at the end of April.

“We continued to significantly increase the Bank’s profitability last year. Now, we need to consolidate the trust we have earned on the capital market”, said Chief Financial Officer Bettina Orlopp. “We want to be an attractive investment. Therefore, we are planning to return around €1 billion to our shareholders for the 2023 financial year. For 2024, we are aiming for a pay-out ratio of at least 70%, but not more than the net result after deduction of AT1 coupon payments. This is an integral part of our strategic plan until 2027, and we will continue to focus on a combination of dividend payments and share buy-backs – the latter subject to the approval of the European Central Bank and the German Finance Agency.”

Development of segments: continued deposit growth

The Private and Small-Business Customer (PSBC) segment in Germany generated revenues of €4.139 billion in the financial year 2023 (2022: €4.318 billion) and an operating result of €878 million (2022: €1.091 billion). The segment’s customer business performed well in the fourth quarter. The lower revenues of €896 million (Q3 2023: €1.046 billion) and the operating result of minus €10 million (Q3 2023: €299 million) largely reflect an on Group level neutral adjustment in the replication portfolio as well as the revaluation of a participation. Excluding these effects, customer revenues in the final quarter remained stable.

The securities volume rose to €215 billion at the end of the year (Q4 2022: €189 billion). The lending volume remained stable at €124 billion (Q4 2022: €124 billion), as did the mortgage volume at €94 billion (Q4 2022: €94 billion). Despite intense competition, customer deposits increased to €166 billion at the end of the year (Q4 2022: €155 billion). Growth in the final quarter totalled €9 billion (Q3 2023: €157 billion).

In Poland, mBank generated revenues of €1.235 billion in the full year 2023 (2022: €948 million) thanks to strong customer business and high interest rates. This enabled it to compensate for the once again high special burdens of €1.094 billion (2022: €650 million) due to provisions for legal risks in connection with Swiss franc loans. In 2023, mBank contributed €146 million to the Group’s operating result (2022: minus €90 million). Without the special burdens due to the additional provisioning for legal risk of Swiss franc mortgages and the so-called credit holidays, mBank would have increased its operating result to €1.228 billion in 2023 (2022: €839 million).

The Corporate Clients segment doubled its operating result to €2.142 billion in 2023 (2022: €1.065 billion). This was due to the favourable interest rate environment, a very low risk result, and reduced costs. In the fourth quarter, customer business remained stable across all customer groups, while valuation effects at the end of the year had a slightly dampening effect on the result. Revenues amounted to €1.106 billion (Q3 2023: €1.171 billion); the operating result totalled €508 million (Q3 2023: €644 million). For the financial year 2023, revenues in the Corporate Clients business increased by 18% to €4.481 billion (2022: €3.792 billion).

Outlook 2024: Important milestones on the way to 2027 targets

The continuing economic slowdown will remain a challenge in the current financial year. Commerzbank is confident that it will make further progress in implementing its strategic plan until 2027. The Bank targets net interest income at around €7.9 billion due to a higher deposit beta and the anticipated interest rate reductions. Commerzbank aims to increase net commission income by 4 %. The Bank is targeting a cost-income ratio of 60%. From today’s perspective, Commerzbank aims for a risk result below minus €800 million for the full year assuming usage of TLA. The CET 1 ratio is expected to be higher than 14% due to planned capital return and RWA growth. The Bank aims for a net profit higher than in 2023.

Based on its capital return policy Commerzbank targets a pay-out ratio of 70 + X% for the financial year 2024, but not more than the net result after deduction of AT1 coupon payments. The capital will be distributed via dividend payments and share buy-backs. All share buy-backs must be authorised by the European Central Bank and the German Finance Agency. The outlook is based on the assumption of a mild recession in Germany and is subject to the future development of Swiss franc loan burdens at mBank.

Press contact

Kathrin Jones

Svea Junge

Contact for investors

Jutta Madjlessi

Michael Klein

Download

About Commerzbank

Commerzbank is the leading bank for the German Mittelstand and a strong partner for around 25,500 corporate client groups and almost 11 million private and small-business customers in Germany. The Bank’s two Business Segments – Private and Small-Business Customers and Corporate Clients – offer a comprehensive portfolio of financial services. Commerzbank transacts approximately 30 per cent of Germany’s foreign trade and is present internationally in more than 40 countries in the corporate clients’ business. The Bank focusses on the German Mittelstand, large corporates, and institutional clients. As part of its international business, Commerzbank supports clients with a business relationship to Germany, Austria, or Switzerland and companies operating in selected future-oriented industries. In the Private and Small-Business Customers segment, the Bank is at the side of its customers with its brands Commerzbank and comdirect: online and mobile, in the advisory centre, and personally in its branches. Its Polish subsidiary mBank S.A. is an innovative digital bank that serves approximately 5.8 million private and corporate customers, predominantly in Poland, as well as in the Czech Republic and Slovakia.

Disclaimer

This release contains forward-looking statements. Forward-looking statements are statements that are not historical facts. In this release, these statements concern inter alia the expected future business of Commerzbank, efficiency gains and expected synergies, expected growth prospects and other opportunities for an increase in value of Commerzbank as well as expected future financial results, restructuring costs and other financial developments and information. These forward-looking statements are based on the management’s current plans, expectations, estimates and projections. They are subject to a number of assumptions and involve known and unknown risks, uncertainties and other factors that may cause actual results and developments to differ materially from any future results and developments expressed or implied by such forward-looking statements. Such factors include the conditions in the financial markets in Germany, in Europe, in the USA and other regions from which Commerzbank derives a substantial portion of its revenues and in which Commerzbank holds a substantial portion of its assets, the development of asset prices and market volatility, especially due to the ongoing European debt crisis, potential defaults of borrowers or trading counterparties, the implementation of its strategic initiatives to improve its business model, the reliability of its risk management policies, procedures and methods, risks arising as a result of regulatory change and other risks. Forward-looking statements therefore speak only as of the date they are made. Commerzbank has no obligation to update or release any revisions to the forward-looking statements contained in this release to reflect events or circumstances after the date of this release.